-

使用tushare包获取某股票的历史行情数据。

-

输出该股票所有收盘比开盘上涨3%以上的日期。

-

输出该股票所有开盘比前日收盘跌幅超过2%的日期。

-

假如我从2010年1月1日开始,每月第一个交易日买入1手股票,每年最后一个交易日卖出所有股票,到今天为止,我的收益如何?

-

tushare:财经数据接口包(免费开源给金融分析人员提供)

-

pip install tushare

-

1、获取某只股票的历史行情数据在tushare官方文档看

import tushare as ts import pandas as pd from pandas import DataFrame,Series import numpy as np

#code:字符串形式的股票代码 df = ts.get_k_data(code='600519',start='2000-01-01') # 此接口不维护了 df

date open close high low volume code 0 2001-08-27 -113.034 -112.849 -112.453 -113.329 406318.00 600519 1 2001-08-28 -112.949 -112.616 -112.591 -113.016 129647.79 600519 2 2001-08-29 -112.595 -112.702 -112.591 -112.751 53252.75 600519 3 2001-08-30 -112.719 -112.574 -112.501 -112.769 48013.06 600519 4 2001-08-31 -112.565 -112.590 -112.481 -112.627 23231.48 600519 ... ... ... ... ... ... ... ... 5074 2022-11-16 1581.000 1585.250 1598.000 1568.000 26848.00 600519 5075 2022-11-17 1590.500 1567.000 1596.300 1552.880 30580.00 600519 5076 2022-11-18 1576.000 1567.130 1584.000 1556.000 23609.00 600519 5077 2022-11-21 1541.350 1519.980 1541.350 1498.530 39096.00 600519 5078 2022-11-22 1517.440 1539.950 1559.740 1516.110 29901.00 600519 5079 rows × 7 columns

#将互联网上获取的股票数据存储到本地(当前目录下) df.to_csv('./maotai1.csv')#调用to_xxx方法将df中的数据写入到本地进行存储 #将本地存储的数据读入到df df = pd.read_csv('./maotai1.csv') df.head()

Unnamed: 0 date open close high low volume code

0 0 2001-08-27 -113.034 -112.849 -112.453 -113.329 406318.00 600519

1 1 2001-08-28 -112.949 -112.616 -112.591 -113.016 129647.79 600519

2 2 2001-08-29 -112.595 -112.702 -112.591 -112.751 53252.75 600519

3 3 2001-08-30 -112.719 -112.574 -112.501 -112.769 48013.06 600519

4 4 2001-08-31 -112.565 -112.590 -112.481 -112.627 23231.48 600519

#需要对读取出来的数据进行相关的处理 #删除df中指定的一列(Unnamed: 0 这一列 axis=1 drop是列) df.drop(labels='Unnamed: 0',axis=1,inplace=True) #查看每一列的数据类型 date列是字符串 df.info()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 5079 entries, 0 to 5078 Data columns (total 7 columns): # Column Non-Null Count Dtype --- ------ -------------- ----- 0 date 5079 non-null object 1 open 5079 non-null float64 2 close 5079 non-null float64 3 high 5079 non-null float64 4 low 5079 non-null float64 5 volume 5079 non-null float64 6 code 5079 non-null int64 dtypes: float64(5), int64(1), object(1) memory usage: 277.9+ KB

#将date列转为时间序列类型 df['date'] = pd.to_datetime(df['date']) df.info()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 5079 entries, 0 to 5078 Data columns (total 7 columns): # Column Non-Null Count Dtype --- ------ -------------- ----- 0 date 5079 non-null datetime64[ns] 1 open 5079 non-null float64 2 close 5079 non-null float64 3 high 5079 non-null float64 4 low 5079 non-null float64 5 volume 5079 non-null float64 6 code 5079 non-null int64 dtypes: datetime64[ns](1), float64(5), int64(1) memory usage: 277.9 KB

#将date列作为源数据的行索引 df.set_index('date',inplace=True) df.head()

open close high low volume code

date

2001-08-27 -113.034 -112.849 -112.453 -113.329 406318.00 600519

2001-08-28 -112.949 -112.616 -112.591 -113.016 129647.79 600519

2001-08-29 -112.595 -112.702 -112.591 -112.751 53252.75 600519

2001-08-30 -112.719 -112.574 -112.501 -112.769 48013.06 600519

2001-08-31 -112.565 -112.590 -112.481 -112.627 23231.48 600519

2、输出该股票所有收盘比开盘上涨3%以上的日期

#伪代码:(收盘-开盘)/开盘 > 0.03 (df['open'] - df['close']) / df['open'] > 0.03 #在分析的过程中如果产生了boolean值 则下一步马上将布尔值 作为源数据的 行索引 #如果布尔值作为df的行索引,则可以取出true对应的行数据,忽略false对应的行数据 df.loc[(df['open'] - df['close']) / df['open'] > 0.03] #获取了True对应的行数据(满足需求的行数据) df.loc[(df['open'] - df['close']) / df['open'] > 0.03].index #df的行数据

DatetimeIndex(['2006-05-29', '2006-11-14', '2006-11-30', '2006-12-11', '2006-12-14', '2006-12-18', '2006-12-29', '2007-01-09', '2007-01-11', '2007-01-12', ... '2021-08-26', '2021-10-18', '2021-12-29', '2022-01-13', '2022-01-28', '2022-03-07', '2022-10-10', '2022-10-19', '2022-10-24', '2022-10-27'], dtype='datetime64[ns]', name='date', length=819, freq=None)

View Code

3、输出该股票所有开盘比前日收盘跌幅超过2%的日期

#伪代码:(开盘-前日收盘)/前日收盘 < -0.02 () (df['open'] - df['close'].shift(1))/df['close'].shift(1) < -0.02 #将布尔值作为源数据的行索引取出True对应的行数据 df.loc[(df['open'] - df['close'].shift(1))/df['close'].shift(1) < -0.02] df.loc[(df['open'] - df['close'].shift(1))/df['close'].shift(1) < -0.02].index

DatetimeIndex(['2006-04-17', '2006-04-18', '2006-04-19', '2006-04-20', '2006-05-25', '2006-05-30', '2007-01-04', '2007-02-16', '2007-03-01', '2007-03-07', ... '2021-02-26', '2021-03-04', '2021-04-28', '2021-08-20', '2021-11-01', '2022-03-14', '2022-03-15', '2022-03-28', '2022-10-13', '2022-10-24'], dtype='datetime64[ns]', name='date', length=451, freq=None)

View Code

4、需求:假如我从2010年1月1日开始,每月第一个交易日买入1手股票,每年最后一个交易日卖出所有股票,到今天为止,我的收益如何?

分析:

-

时间节点:2010-2020

-

一手股票:100支股票

-

买:

-

一个完整的年需要买入1200支股票

-

-

卖:

-

一个完整的年需要卖出1200支股票

-

-

买卖股票的单价:

-

开盘价

-

new_df = df['2010-01':'2020-02'] new_df new_df.head(2)

open close high low volume code

date

2010-01-04 109.760 108.446 109.760 108.044 44304.88 600519

2010-01-05 109.116 108.127 109.441 107.846 31513.18 600519

View Code

#买股票操作:首先找每个月的第一个交易日对应的行数据(捕获到开盘价)==》每月的第一行数据 #根据月份从原始数据中提取指定的数据resample('M') #first()每月第一个交易日对应的行数据 df_monthly = new_df.resample('M').first()#resample数据的重新取样 M根据月份 df_monthly #买入股票花费的总金额 cost = df_monthly['open'].sum()*100 cost

4010206.1

#卖出股票到手的钱 #特殊情况:当前时间是2020年 2020年买入的股票卖不出去 new_df.resample('A').last() #将2020年最后一行切出去取数据到2019年 df_yearly = new_df.resample('A').last()[:-1] df_yearly

open close high low volume code

date

2010-12-31 117.103 118.469 118.701 116.620 46084.0 600519

2011-12-31 138.039 138.468 139.600 136.105 29460.0 600519

2012-12-31 155.208 152.087 156.292 150.144 51914.0 600519

2013-12-31 93.188 96.480 97.179 92.061 57546.0 600519

2014-12-31 157.642 161.056 161.379 157.132 46269.0 600519

2015-12-31 207.487 207.458 208.704 207.106 19673.0 600519

2016-12-31 317.239 324.563 325.670 317.239 34687.0 600519

2017-12-31 707.948 687.725 716.329 681.918 76038.0 600519

2018-12-31 563.300 590.010 596.400 560.000 63678.0 600519

2019-12-31 1183.000 1183.000 1188.000 1176.510 22588.0 600519

View Code

#卖出股票到手的钱 resv = df_yearly['open'].sum()*1200 resv 4368184.8 #最后手中剩余的股票需要估量其价值计算到总收益中 #使用昨天的收盘价作为剩余股票的单价 last_monry = 200*new_df['close'][-1] #计算总收益 resv+last_monry-cost

574778.6999999997

需求:双均线策略制定

1、使用tushare包获取某股票的历史行情数据

# 读取茅台股票数据,并删除无用数据列Unnamed: 0 df = pd.read_csv('./maotai.csv').drop(labels='Unnamed: 0',axis=1) df

date open close high low volume code 0 2001-08-27 -113.034 -112.849 -112.453 -113.329 406318.00 600519 1 2001-08-28 -112.949 -112.616 -112.591 -113.016 129647.79 600519 2 2001-08-29 -112.595 -112.702 -112.591 -112.751 53252.75 600519 3 2001-08-30 -112.719 -112.574 -112.501 -112.769 48013.06 600519 4 2001-08-31 -112.565 -112.590 -112.481 -112.627 23231.48 600519 ... ... ... ... ... ... ... ... 5076 2022-11-18 1576.000 1567.130 1584.000 1556.000 23609.00 600519 5077 2022-11-21 1541.350 1519.980 1541.350 1498.530 39096.00 600519 5078 2022-11-22 1517.440 1539.950 1559.740 1516.110 29901.00 600519 5079 2022-11-23 1528.000 1549.000 1557.000 1521.040 22177.00 600519 5080 2022-11-24 1559.000 1519.990 1568.880 1513.980 27687.00 600519 5081 rows × 7 columns

View Code

#将date列转为时间序列且将其作为源数据的行索引 df['date'] = pd.to_datetime(df['date']) df.set_index('date',inplace=True) df.head()

open close high low volume code

date

2001-08-27 -113.034 -112.849 -112.453 -113.329 406318.00 600519

2001-08-28 -112.949 -112.616 -112.591 -113.016 129647.79 600519

2001-08-29 -112.595 -112.702 -112.591 -112.751 53252.75 600519

2001-08-30 -112.719 -112.574 -112.501 -112.769 48013.06 600519

2001-08-31 -112.565 -112.590 -112.481 -112.627 23231.48 600519

View Code

2、计算该股票历史数据的5日均线和30日均线

-

什么是均线?

-

对于每一个交易日,都可以计算出前N天的移动平均值,然后把这些移动平均值连起来,成为一条线,就叫做N日移动平均线。移动平均线常用线有5天、10天、30天、60天、120天和240天的指标。

-

5天和10天的是短线操作的参照指标,称做日均线指标;

-

30天和60天的是中期均线指标,称做季均线指标;

-

120天和240天的是长期均线指标,称做年均线指标。

-

-

-

均线计算方法:MA=(C1+C2+C3+…+Cn)/N C:某日收盘价 N:移动平均周期(天数)

# 取close列 rolling(5)把每五天取值mean()取均值 ma5 = df['close'].rolling(5).mean() # 30日均线 ma30 = df['close'].rolling(30).mean()

ma5 date 2001-08-27 NaN 2001-08-28 NaN 2001-08-29 NaN 2001-08-30 NaN 2001-08-31 -112.6662 ... 2022-11-18 1568.0760 2022-11-21 1565.4720 2022-11-22 1555.8620 2022-11-23 1548.6120 2022-11-24 1539.2100 Name: close, Length: 5081, dtype: float64 ma30 date 2001-08-27 NaN 2001-08-28 NaN 2001-08-29 NaN 2001-08-30 NaN 2001-08-31 NaN ... 2022-11-18 1561.499667 2022-11-21 1552.632333 2022-11-22 1544.631000 2022-11-23 1537.597667 2022-11-24 1531.597667 Name: close, Length: 5081, dtype: float64

View Code

# 将均线画出 import matplotlib.pyplot as plt %matplotlib inline # 画线 plt.plot(ma5[50:180]) plt.plot(ma30[50:180])

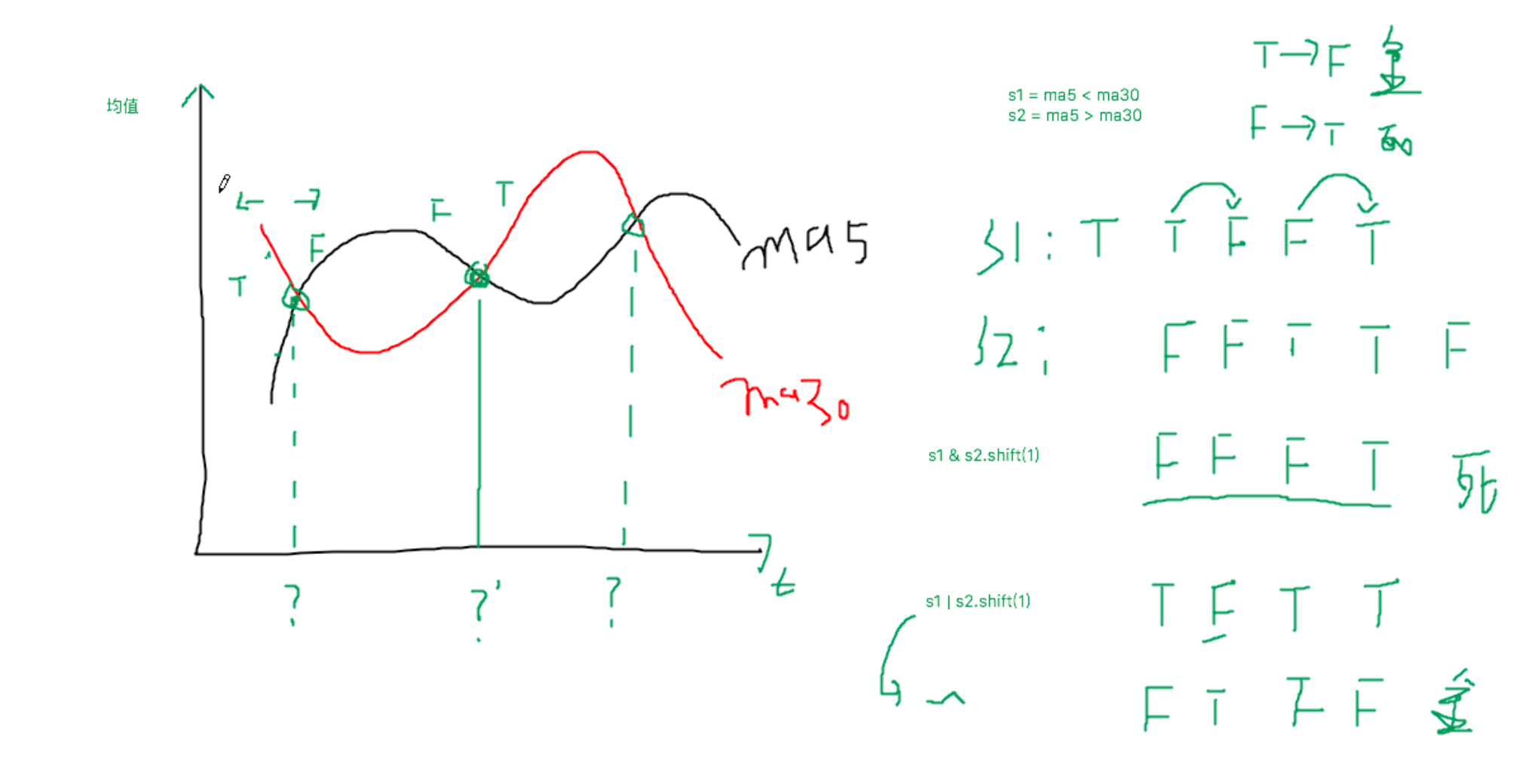

3、分析输出所有金叉日期和死叉日期

-

股票分析技术中的金叉和死叉,可以简单解释为:

-

分析指标中的两根线,一根为短时间内的指标线,另一根为较长时间的指标线。

-

如果短时间的指标线方向拐头向上,并且穿过了较长时间的指标线,这种状态叫“金叉”;

-

如果短时间的指标线方向拐头向下,并且穿过了较长时间的指标线,这种状态叫“死叉”;

-

一般情况下,出现金叉后,操作趋向买入;死叉则趋向卖出。当然,金叉和死叉只是分析指标之一,要和其他很多指标配合使用,才能增加操作的准确性。

-

# ma5 均值就是y轴 ma5 = ma5[30:] ma30 = ma30[30:] s1 = ma5 < ma30 s2 = ma5 > ma30 s1 # true代表ma5 < ma30

date 2001-10-15 True 2001-10-16 True 2001-10-17 True 2001-10-18 True 2001-10-19 True ... 2022-11-18 False 2022-11-21 False 2022-11-22 False 2022-11-23 False 2022-11-24 False Name: close, Length: 5051, dtype: bool

View Code

df = df[30:] # shift(1)往后移一位 death_ex = s1 & s2.shift(1) #判定死叉的条件 如图s1和s2后移动1位的布尔值进行逻辑运算 df.loc[death_ex] #死叉对应的行数据 death_date = df.loc[death_ex].index # 死叉对应时间 golden_ex = ~(s1 | s2.shift(1))#判定金叉的条件 golden_date = df.loc[golden_ex].index #金叉的时间

4、如果我从假如我从2010年1月1日开始,初始资金为100000元,金叉尽量买入,死叉全部卖出,则到今天为止,我的炒股收益率如何?

-

分析:

-

买卖股票的单价使用开盘价

-

买卖股票的时机

-

最终手里会有剩余的股票没有卖出去

-

会有。如果最后一天为金叉,则买入股票。估量剩余股票的价值计算到总收益。

-

剩余股票的单价就是用最后一天的收盘价。

-

-

-

s1 = Series(data=1,index=golden_date) #1作为金叉的标识 s2 = Series(data=0,index=death_date) #0作为死叉的标识 s1

date 2001-11-22 1 2002-01-24 1 2002-02-04 1 2002-06-21 1 2002-12-05 1 .. 2021-11-23 1 2022-04-07 1 2022-06-02 1 2022-09-29 1 2022-11-18 1 Length: 108, dtype: int64

View Code

s = s1.append(s2) # 金叉和死叉交替 s = s.sort_index() #存储的是金叉和死叉对应的时间 s = s['2010':'2020']##存储的是金叉和死叉对应的时间 first_monry = 100000 #本金,不变 money = first_monry #可变的,买股票话的钱和卖股票收入的钱都从该变量中进行操作 hold = 0 #持有股票的数量(股数:100股=1手) for i in range(0,len(s)): #i表示的s这个Series中的隐式索引 #i = 0(死叉:卖) = 1(金叉:买) if s[i] == 1:#金叉的时间 #基于100000的本金尽可能多的去买入股票 #获取股票的单价(金叉时间对应的行数据中的开盘价) time = s.index[i] #金叉的时间 p = df.loc[time]['open'] #股票的单价 开盘价open hand_count = money // (p*100) #使用100000最多买入多少手股票 hold = hand_count * 100 # 多少支股票 money -= (hold * p) #将买股票话的钱从money中减去 else: #将买入的股票卖出去 #找出卖出股票的单价 death_time = s.index[i] p_death = df.loc[death_time]['open'] #卖股票的单价 money += (p_death * hold) #卖出的股票收入 加入到money hold = 0 #如何判定最后一天为金叉还是死叉 last_monry = hold * df['close'][-1] #剩余股票的价值 #总收益 money + last_monry - first_monry

1501254.9999999995

聚宽(这是个学习平台)

原文地址:http://www.cnblogs.com/erhuoyuan/p/16926346.html